Last Updated: March 29, 2026 | Read Time: 11 minutes

The national average for full truck coverage is $222 per month. The cheapest company charges $84. The cheapest truck to insure costs $176 a month. Here is everything you need to know to pay as little as possible — with honest numbers from 2026 data, not estimates from two years ago.

Contents

Cheapest Truck Insurance

– National Average Full Coverage (truck): $222/month — $2,669/year

– National Average Liability Only (truck): $107/month — $1,284/year

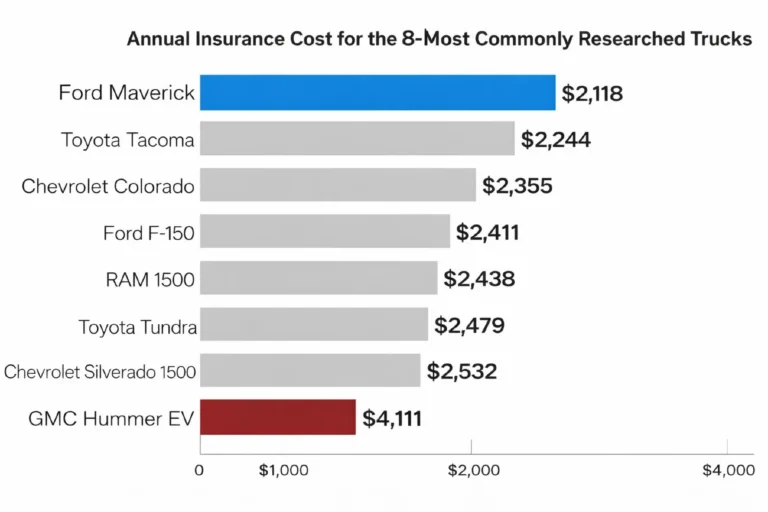

– Cheapest Truck to Insure: Ford Maverick — $2,118/year ($176/month)

– Second Cheapest Truck to Insure: Ford Ranger — $2,156/year ($180/month)

– Most Expensive Truck to Insure: GMC Hummer EV — $4,111/year ($343/month)

– Cheapest Company Overall (personal truck): Auto-Owners — $84/month full coverage

– Second Cheapest: GEICO — $91/month

– USAA (military members only): Starting at $95/month for F-Series trucks

– Cheapest Full-Size Truck: Ford F-150 — approximately $191/month full coverage

– Trucks vs. Cars: Trucks cost 6% more than cars to insure on average — but less than many sedans on a model-by-model basis

– Cheapest State for Personal Truck Insurance: Vermont — consistently lowest rates

– Most Expensive State: Louisiana — highest rates nationally

Sources: Insure.com (February 2026), Insurify (February 2026), MoneyGeek (February 2026), The Zebra (January 2026), Logrock (February 2026)

Why Truck Insurance Is More Complicated Than It Looks — And How To Win Anyway

Most people think truck insurance is simple. You buy a truck, you call your insurer, you add it to your policy, and you pay whatever they tell you. End of story.

That approach works. It also costs more money than it needs to every single month for the life of the truck, and most people never realize it because they never had the information they needed to push back.

Here is the core truth about truck insurance in 2026: the same coverage for the same truck can cost $84 a month from one company or $180 a month from another. That is not a small difference. Over a five-year ownership period, that gap compounds to $5,760 — enough to cover more than a year’s worth of fuel, a set of premium tires, or several months of truck payments. The difference between those two numbers is not the coverage — it is the company you chose, the truck you drive, and whether you knew what questions to ask.

The second truth is that trucks are not automatically expensive to insure. The narrative that trucks cost more than cars to insure is technically true on average — full-coverage truck insurance averages $222 per month, more than 6% higher than the national average for cars — but it masks enormous variation within the truck category itself. The Ford Maverick averages $2,118 per year to insure, while the GMC Hummer EV Truck costs about $4,111 annually. That is a $2,000 annual difference between two vehicles both classified as pickup trucks. The truck category is not monolithic. Your specific truck matters enormously.

The third truth — and the one that most insurance content ignores — is that what you pay is substantially within your control. The company you choose, the coverage you select, the deductible you set, the discounts you claim, and the driving record you maintain are all levers you can pull. This guide shows you exactly how to pull them.

Truck insurance does not exist in isolation — it is part of a broader auto insurance market that has increased 22% since 2022. Our complete breakdown of car insurance cost in the USA in 2026 gives you the national framework, the state-by-state breakdown, and every factor that has driven rates higher across all vehicle types including trucks.

This article covers personal pickup truck insurance — the kind everyday drivers carry on their personal F-150, Silverado, Ranger, or Tacoma. If you use a truck for business — hauling freight, running a commercial route, or operating as an owner-operator — that conversation is different and is addressed in a dedicated section.

Which Pickup Trucks Cost The Least To Insure In 2026

If you haven’t bought your truck yet, this section is the most valuable one in the guide. Insurance cost is a significant ongoing expense that most truck buyers never factor into their purchase decision — and it should be, because the difference between the cheapest and most expensive trucks to insure is more than $2,000 per year.

Here are the trucks that cost the least to insure in 2026, based on Insure.com’s analysis of 67.5 million insurance quotes from 57 companies.

The Ford Maverick — Cheapest Truck To Insure: $2,118/Year ($176/Month)

The Ford Maverick and Ford Ranger are the cheapest trucks to insure at $2,118 and $2,156 annually, respectively. The Maverick’s position at the top of the cheapest list comes from a combination of factors that any insurance actuary would predict: it is the smallest, lightest, and least powerful pickup in Ford’s lineup, with a standard hybrid powertrain, excellent safety ratings, and repair costs that are meaningfully lower than full-size trucks.

The Maverick starts at approximately $23,495 with the standard hybrid powertrain — the most affordable new truck available in America — and its modest power output and front-wheel-drive standard configuration contribute to an insurance risk profile that insurers price favorably. For buyers who need a truck’s cargo and towing capability but not necessarily a full-size platform, the Maverick represents a genuinely compelling combination of low purchase price and low insurance cost. The total cost of ownership argument for the Maverick is, in 2026, one of the strongest in any vehicle segment.

The Ford Ranger — Second Cheapest: $2,156/Year ($180/Month)

The Ford Ranger’s $180 monthly average puts it almost exactly level with the Maverick. The Ranger is a midsize truck — larger than the Maverick but significantly smaller and lighter than the F-150 — and its insurance cost reflects the midsize truck category’s generally favorable insurance profile. The Colorado, Canyon, and Ranger consistently appear at the low end of truck insurance cost tables across multiple data sources for 2026.

For buyers who need more capability than the Maverick offers but want to keep insurance costs controlled, the Ranger is the correct choice. The insurance advantage over the full-size F-150 typically runs $10 to $30 per month — meaningful over a full ownership period.

The Chevrolet Colorado And GMC Canyon

The Colorado and Canyon — effectively the same truck under different badges — rank alongside the Ranger as among the cheapest midsize trucks to insure in 2026. The Chevrolet Colorado, GMC Canyon, and Ford Ranger are among the cheapest to insure in the pickup category, according to The Zebra’s 2026 analysis. Their competitive repair costs, strong safety ratings, and midsize dimensions all contribute to favorable insurance pricing.

The Ford F-150 — Cheapest Full-Size Truck: $191/Month

The Ford F-150 truck has a starting MSRP of $37,065 and costs around $191 per month for full coverage, on average. Among full-size trucks, the F-150 is consistently one of the cheapest to insure — a fact that surprises many buyers who assume the best-selling truck in America would carry higher insurance costs. The F-150’s strong IIHS safety ratings are a primary driver of its favorable insurance pricing: insurers price based on claim frequency and severity, and well-rated safety systems reduce both.

The Ford F-150 is one of the cheapest full-size pickups to insure. For the overwhelming majority of buyers choosing a full-size truck in 2026, the F-150’s combination of purchase price, capability, and insurance cost makes it the financially rational choice within its segment.

The Most Expensive Trucks To Insure — What To Avoid If Cost Is A Priority

At the other end of the spectrum, several trucks carry insurance costs that should give budget-conscious buyers pause. The GMC Hummer EV Truck is the most expensive vehicle to insure, averaging $4,111 per year — nearly double the Maverick’s annual cost. The Hummer EV’s high repair costs, expensive replacement parts, and significant vehicle value all drive its insurance premium. High-performance truck variants — lifted editions, performance packages, and heavily optioned trims — also carry insurance premiums that can be 20 to 40 percent higher than the base trim of the same model.

If minimizing insurance cost is a priority, the rule is straightforward: smaller truck, lower trim, standard powertrain. Every step away from that baseline increases the premium.

Which Company Charges The Least For Pickup Truck Coverage In 2026

Auto-Owners Insurance — Cheapest Full Coverage: $84/Month

Auto-Owners offers the cheapest pickup truck insurance at $84 monthly for full coverage. Auto-Owners is a regional insurer that operates primarily in the Midwest and Southeast — not available in all states, but where it is available, it consistently offers rates that are difficult for national carriers to match for truck owners with clean driving records.

If you live in a state where Auto-Owners operates, getting a quote from them is not optional — it is the first step in any intelligent truck insurance shopping process. The $84 monthly figure represents their best case for a qualified driver, but even their average rates are among the lowest in the industry for personal truck coverage.

Auto-Owners currently operates in 26 states. States include Alabama, Arizona, Arkansas, Colorado, Florida, Georgia, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Mississippi, Missouri, Nebraska, North Carolina, North Dakota, Ohio, Pennsylvania, South Carolina, South Dakota, Tennessee, Virginia, and Wisconsin. If you live in one of these states and have not gotten an Auto-Owners quote, you are almost certainly overpaying.

GEICO — Second Cheapest: $91/Month

GEICO, Travelers, Erie and Progressive charge $91 to $120 for pickup truck full coverage. GEICO’s $91 monthly average makes it the most accessible cheap option for truck owners nationally — unlike Auto-Owners, GEICO operates in all 50 states and D.C. For truck owners who live outside Auto-Owners’ coverage area, GEICO is typically the first company to benchmark against.

GEICO’s rates are competitive across most driver profiles, though they are particularly favorable for drivers with clean records, higher credit scores, and trucks in the base-to-mid trim range. GEICO’s mobile app and digital claims process are among the best in the industry, which matters when you are actually using the insurance rather than just shopping for it.

USAA — Cheapest For Military Members And Families: Starting At $95/Month

USAA offers the cheapest monthly rates for truck insurance. For active military, veterans, and their immediate family members, USAA is the benchmark that every other company competes against — and frequently loses. USAA offers the cheapest truck insurance monthly rate for the F-Series, starting at $95.

The qualification requirement — current or former military service, or immediate family member of a qualifying member — means USAA is not available to most truck owners. But for those who qualify, the combination of rates, customer service, and claims handling makes USAA the clear first choice. If you qualify and are not currently insured with USAA, get a quote immediately. The savings compared to national averages are consistently significant.

Travelers — $96 To $120/Month

Travelers is one of the largest personal lines insurers in the United States and consistently ranks among the cheaper options for truck insurance, particularly for drivers with clean records and trucks in the three-to-seven-year age range. Their IntelliDrive telematics program — which monitors driving behavior and adjusts rates based on actual driving data — can produce additional savings of up to 30 percent for drivers who are genuinely low-risk.

Travelers is available nationally and their truck-specific pricing is competitive enough to benchmark in any shopping process. Their claims service is well-regarded, which is the second most important factor after price for any insurance purchase.

Erie Insurance — Competitive At $97 To $115/Month

Erie Insurance operates in the Mid-Atlantic, Midwest, and Southeast — not national, but where it operates, its rates are consistently competitive and its customer service ratings are among the highest of any major insurer. Erie’s Rate Lock program — which guarantees your rate won’t increase at renewal unless you change your policy — is a genuinely unusual and valuable feature for truck owners concerned about rate creep over time.

Progressive — $110 To $130/Month — Best For High-Risk Profiles

Progressive’s rates for standard truck insurance are not the lowest among the major national carriers, but Progressive is worth noting specifically for drivers who don’t qualify for the best rates elsewhere — those with recent accidents, violations, or gaps in coverage. Progressive is consistently more willing to write policies for higher-risk profiles than competitors, and their Snapshot telematics program offers meaningful discounts for drivers who can demonstrate safe behavior over a monitoring period.

For the commercial side, Progressive offers the lowest rates across all seven vehicle types in the commercial truck space. If you use your truck for business purposes, Progressive Commercial deserves specific attention.

What You Actually Need And What You’re Paying For

Liability Only Coverage — $107/Month National Average

The average national monthly payment for trucks is $107 for liability-only insurance and $198 for full coverage. Liability coverage pays for damage you cause to other vehicles, property, or people in an accident where you are at fault. It does not pay to repair or replace your own truck. Every state except New Hampshire requires a minimum amount of liability coverage as a condition of vehicle registration.

Liability only is appropriate for older trucks with low market value — specifically, trucks where the cost of adding collision and comprehensive coverage exceeds a reasonable percentage of the truck’s actual cash value. The general guideline: if your truck is worth less than $6,000 to $8,000 on the used market, liability-only coverage is often the financially rational choice.

For newer trucks, financed trucks, or leased trucks, liability only is typically not an option — lenders require full coverage as a condition of the loan or lease.

Full Coverage — $222/Month National Average

Full coverage means liability plus collision plus comprehensive. Collision coverage pays for damage to your truck from a collision with another vehicle or object. Comprehensive coverage pays for damage from non-collision events — theft, fire, weather, falling objects, animal strikes, and vandalism.

It costs an average of $222 per month to insure a truck or $2,669 annually. That figure is the national average across all trucks and all drivers. Your actual rate will be higher or lower depending on your specific truck, driving history, location, age, credit score, and coverage limits. The specific variables that move the needle are covered below in the text.

For any truck financed or leased in the last five years, full coverage is almost certainly required by your lender. For paid-off trucks, the decision between full and liability only should be made by comparing the annual cost of full coverage against the truck’s actual cash value — the number your insurer would pay if the truck were totaled.

Gap Coverage — Often Worth Adding On New Trucks

Gap insurance covers the difference between what you owe on a truck loan and what the truck is actually worth if it is totaled. New trucks depreciate rapidly — a truck financed at $55,000 may be worth $40,000 twelve months later, while the loan balance has only decreased to $50,000. Without gap coverage, you would owe $10,000 out of pocket after a total loss.

Gap coverage typically costs $20 to $40 per month when added through an insurer — significantly less than the $500 to $1,000 that dealerships typically charge for the same coverage when rolled into the financing. Never buy gap coverage at the dealership. Buy it from your insurer.

The Nine Factors That Determine What You Actually Pay

Understanding these variables lets you predict your rate before you shop and identify which levers you can pull to reduce it.

Your Driving Record

This is the single most powerful factor in your insurance rate. A clean driving record — no at-fault accidents, no moving violations, no DUI — is the baseline that qualifies you for the best rates any company offers. A single at-fault accident raises your premium on average by 43 percent. A DUI raises it by 96 percent on average and can persist on your record for three to five years depending on state. Speeding tickets typically raise rates by 20 to 25 percent each.

The practical implication: your insurance rate is largely a direct financial consequence of how you drive. Every year with a clean record is a year of rate improvement. Every at-fault incident resets the clock.

Your Age

Insurance rates peak for drivers under 25 — particularly males under 25. Rates decline consistently from age 25 through approximately 65, then begin to rise again for senior drivers. A 21-year-old male driving the same truck with the same record as a 40-year-old male will pay significantly more — often 60 to 100 percent more — for identical coverage from the same company.

If you have a young driver on your policy, adding them to the household policy rather than giving them their own separate policy is almost always less expensive. Adding a teen to a family policy averages $2,500 to $5,000 per year — significant, but less than a standalone policy for a young driver.

If the young driver on your policy is getting their first vehicle, the truck is almost never the right choice from an insurance cost perspective — our guide to the best first cars for teenagers in 2026 covers specifically why smaller, lower-powered American vehicles produce dramatically lower insurance costs for new drivers than any full-size or performance truck.

Your Credit Score

In most states, insurance companies use a credit-based insurance score — related to but not identical to your standard credit score — as a pricing factor. The correlation between credit score and claim frequency is documented across the industry. Poor credit raises truck insurance premiums by 60 to 80 percent on average compared to good credit.

States that prohibit credit-based insurance scoring include California, Hawaii, Massachusetts, and Michigan. In all other states, improving your credit score is one of the highest-leverage financial moves available for reducing your insurance premium over time.

Your Location

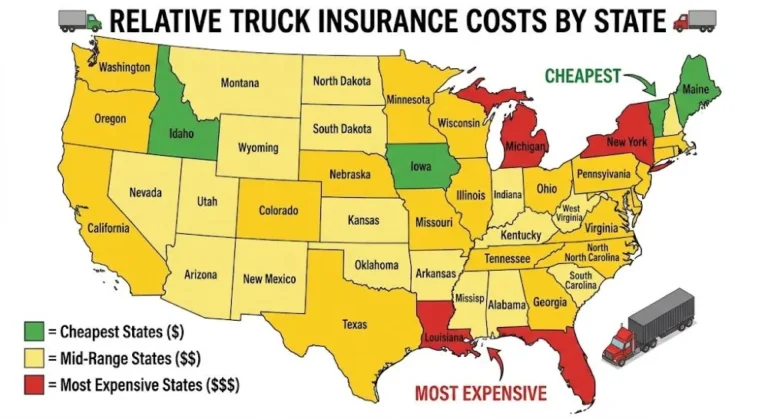

Where you garage your truck overnight is a more powerful pricing factor than many drivers realize. Urban ZIP codes carry higher rates than suburban or rural areas due to higher traffic density, higher theft rates, and higher claim frequencies. Within the same state, the premium difference between an urban and rural address can be 25 to 40 percent. State-level differences are even more pronounced — Vermont is consistently among the cheapest states for personal truck insurance while Louisiana is consistently the most expensive.

Your Truck’s Age, Trim, And Value

Newer, more expensive trucks cost more to insure because they cost more to repair and replace. The comprehensive and collision portions of your premium are directly tied to your truck’s actual cash value — as the truck ages and depreciates, these portions decrease proportionally. Trim level matters too: a heavily optioned truck with advanced technology features costs significantly more to repair after an accident than a base-trim equivalent.

Your Annual Mileage

Higher mileage means more exposure — more time on the road means more opportunity for an accident. Most insurers offer low-mileage discounts for drivers under 7,500 to 10,000 miles annually. If you work from home, have a short commute, or keep a second vehicle for most driving, reporting your accurate low mileage can produce meaningful savings.

Your Coverage Limits And Deductibles

Higher liability limits cost more. Higher collision and comprehensive deductibles cost less. The relationship between deductible level and premium is direct — raising your collision deductible from $500 to $1,000 typically reduces your collision premium by 10 to 15 percent. Raising it to $2,000 can reduce it by 20 to 25 percent. The trade-off is that you pay more out of pocket in a claim. Choose the deductible level at which you can cover the cost without financial hardship.

Nine Proven Strategies To Lower Your Truck Insurance In 2026

Strategy 1: Shop Every Renewal — Without Exception

The most important action any truck owner can take is to compare rates from at least three to five companies every year at renewal time. Insurance companies regularly change their pricing models, and the company that was cheapest for you two years ago may not be cheapest today. Compare at least three quotes to find rates ranging from $200 to $500 monthly. Companies like Progressive Commercial and GEICO price identical coverage differently based on their risk models.

Use online comparison tools to get multiple quotes simultaneously. Then call the top two or three results to confirm coverage is identical before comparing prices. The 30 minutes this takes annually can produce savings of $300 to $1,500 per year for the same coverage level.

Strategy 2: Bundle Your Truck With Home Or Renters Insurance

Most major insurers offer a multi-policy discount of 5 to 25 percent when you bundle auto with home, renters, or life insurance. If your truck and home are with different companies, you are almost certainly leaving money on the table. Get a bundled quote from both your current auto insurer and your current home insurer and compare the total combined cost. The savings from bundling consistently outweigh loyalty to either carrier individually.

Strategy 3: Install A Telematics Device And Drive Well

GEICO’s DriveEasy, Progressive’s Snapshot, Travelers’ IntelliDrive, and State Farm’s Drive Safe and Save all offer discounts of 10 to 30 percent for drivers who allow their insurer to monitor driving behavior through a phone app or plug-in device. If you are a genuinely low-risk driver — smooth acceleration, no hard braking, no late-night driving — telematics programs are free money. The monitoring period is typically 30 to 90 days after which the discount is locked in.

If you know you are not a smooth driver, skip telematics programs — they can occasionally raise rates for high-risk driving behavior in some programs.

Strategy 4: Increase Your Deductible

If your emergency fund can absorb the out-of-pocket cost of a higher deductible in a claim scenario, raising your deductible is one of the fastest and most reliable ways to reduce your premium immediately. Going from a $500 to a $1,000 deductible typically reduces your collision and comprehensive premium by 10 to 15 percent. Going to $2,000 can save 20 to 25 percent. This strategy makes the most sense on trucks that are three years or older, where the risk of a total loss has diminished and the annual premium savings compound meaningfully over time.

Strategy 5: Ask For Every Discount You Qualify For

Insurance companies do not automatically apply all discounts you qualify for — you have to ask. Common discounts that truck owners regularly miss include the good student discount (for young drivers on the policy with a GPA of 3.0 or higher), the defensive driving course discount, the anti-theft device discount, the good driver discount (varies by company but typically requires 3 to 5 clean years), the vehicle safety features discount, the paid-in-full discount for paying annually rather than monthly, and the paperless billing discount. Asking specifically for a discount review at renewal is a free, five-minute conversation that can save $50 to $300 per year.

Strategy 6: Maintain Continuous Coverage — Never Let It Lapse

A gap in insurance coverage — even a short one — signals risk to insurers and can raise your rate by 15 to 30 percent at your next policy. Insurers treat coverage gaps as an indicator of financial instability or undisclosed risk. If you sell a truck and plan to be without a vehicle temporarily, consider a non-owner auto policy to maintain continuous coverage on your record until your next vehicle purchase.

Strategy 7: Choose The Right Truck Before You Buy

The cheapest truck to insure is $2,118 per year. The most expensive is $4,111. That $1,993 annual difference is entirely determined by which truck you choose. Before you purchase any new or used truck, get an insurance quote for that specific vehicle from your current insurer. The quote takes five minutes online and can prevent years of unnecessarily high premiums.

Strategy 8: Improve Your Credit Score

In states where credit-based insurance scoring is permitted, improving your credit score from fair to good can reduce your insurance premium by 25 to 40 percent over time. This is not an immediate fix — credit improvement takes months and years. But for truck owners who plan to own and insure a vehicle long-term, the insurance dividend from credit improvement is real and measurable.

Strategy 9: Review Your Coverage On Older Trucks Annually

A truck that was worth $40,000 when you bought it full coverage for is now worth $18,000. You may still be paying premiums calibrated to the original value. Review your truck’s actual cash value annually — the Kelly Blue Book private party value is a reasonable proxy — and compare the annual cost of collision and comprehensive coverage against that value. When the ratio exceeds approximately 10 percent annually, dropping collision and comprehensive coverage and moving to liability only may be financially rational.

When deciding whether full coverage is worth keeping on an older truck, consider all the costs of a potential claim — including paint and body repair work, which has increased significantly in recent years. Our guide to how much it costs to paint a car in 2026 breaks down exactly what a single-panel repair to a full-body respray runs in today’s market, helping you calculate whether your deductible and premium make financial sense.

When Personal Coverage Is Not Enough: Commercial Truck Insurance Explained

If you use your truck for business purposes — hauling freight, operating as a contractor, running deliveries, or any commercial use — your personal auto insurance policy almost certainly does not cover you. Most personal auto policies contain explicit exclusions for commercial use, meaning a claim arising from business use of the vehicle can be denied entirely.

The commercial truck insurance market is a fundamentally different conversation from personal pickup truck insurance. Pickup trucks cost the least to insure at $209 monthly on average, with rates starting as low as $41 for state minimum coverage. HAZMAT tankers run $959, nearly five times more. Progressive offers the lowest rates across all seven vehicle types.

For owner-operators running under their own authority, the cost reality is considerably higher. In 2026, many owner-operators who need broker-ready limits budget roughly $900–$1,800+/month, while new authority commonly prices around $1,200–$2,500+/month for a single interstate truck. These numbers reflect the $1 million liability requirement that most freight brokers and shippers require as a condition of working with an owner-operator — a requirement that is separate from state minimum liability limits and that drives commercial truck insurance into a completely different cost tier.

The most important commercial truck insurance company by market share is Progressive Commercial, which offers the lowest rates across all seven vehicle types according to MoneyGeek’s 2026 analysis. The Hartford and Nationwide follow. For owner-operators and small fleets, working with an independent agent who specializes in trucking insurance — rather than going direct to a carrier — provides access to multiple markets and typically produces better results than single-carrier quotes.

Truck Insurance By State: Where You Live Matters More Than You Think

State-level insurance cost variation is one of the most powerful and least-discussed factors in truck insurance pricing. The same truck, the same driver, the same coverage — in different states, the premium can vary by 50 to 100 percent.

New York hits you with $666 monthly for commercial coverage. Maine charges just $275 monthly. While those figures are commercial rates, the geographic pricing differential pattern applies equally to personal truck insurance. In personal truck coverage, Vermont and Maine consistently rank as the cheapest states. Louisiana, Florida, and Michigan consistently rank as the most expensive.

The factors that drive state-level variation include: the state’s minimum liability requirements (higher minimums mean higher baseline costs), the density of uninsured drivers in the state (higher uninsured driver rates raise premiums for everyone), the frequency and severity of weather events that generate comprehensive claims (hailstorm-prone states like Colorado and Kansas see higher comprehensive premiums), and the state’s legal environment for auto insurance litigation (states with more plaintiff-friendly courts see higher premiums across the board).

If you are relocating and own a truck, getting insurance quotes for your new location before you move provides a realistic picture of the cost change. Moving from Louisiana to Vermont with a truck could reduce your annual premium by $800 to $1,500 for identical coverage.

FAQ

Q: What is the cheapest truck to insure in 2026?

A: The Ford Maverick is the cheapest truck to insure in 2026, averaging $2,118 per year or approximately $176 per month for full coverage according to Insure.com’s analysis of 67.5 million insurance quotes. The Ford Ranger is the second cheapest at $2,156 per year. Both are significantly less expensive to insure than full-size trucks. The most expensive truck to insure is the GMC Hummer EV at $4,111 per year — nearly double the Maverick’s cost.

Q: What is the cheapest truck insurance company in 2026?

A: For personal pickup truck insurance, Auto-Owners offers the cheapest full coverage at $84 per month, according to MoneyGeek’s February 2026 analysis. Auto-Owners operates in 26 states. For drivers outside Auto-Owners’ coverage area, GEICO at $91 per month and Travelers at approximately $96 to $120 per month are the next cheapest options nationally. For military members and their families, USAA offers rates starting at $95 per month for F-Series trucks and is consistently the benchmark for the best truck insurance rates in its eligible population.

Q: How much is truck insurance per month on average in 2026?

A: The national average for full-coverage truck insurance is $222 per month or $2,669 per year, according to Insure.com’s February 2026 data. Liability-only coverage averages $107 per month nationally. These are averages across all trucks, all ages, and all states — your actual rate will be higher or lower based on your specific vehicle, driving record, location, age, and coverage level.

Q: Is truck insurance more expensive than car insurance?

A: On average, yes — but by less than most people assume. Full-coverage truck insurance is about 6 percent more expensive than the national average for cars. However, on a model-by-model comparison, many trucks insure for less than popular sedans. The Ford F-150 at $191 per month full coverage is cheaper than the Toyota Camry at $223 per month despite the Camry’s significantly lower purchase price. The F-150’s strong safety ratings are a primary reason for this counterintuitive result.

Q: Does a 4×4 truck cost more to insure?

A: Yes — a 4×4 or AWD truck typically costs more to insure than a 2WD equivalent. The additional drivetrain components increase repair costs, and 4×4 trucks are statistically more likely to be used in off-road or challenging driving conditions that increase claim risk. The premium difference between a 2WD and 4WD version of the same truck model is typically $15 to $35 per month for full coverage.

Q: How can I get the cheapest truck insurance?

A: The most effective strategies for getting cheap truck insurance in 2026 are: comparing quotes from at least three to five companies at every renewal, bundling your truck with home or renters insurance for a multi-policy discount, using a telematics safe driver program if you drive conservatively, increasing your deductible if your emergency fund can absorb it, maintaining continuous coverage without lapses, choosing a truck model that is inexpensive to insure before you buy, and asking your insurer specifically for a discount review at every renewal. Combining multiple strategies simultaneously produces the largest savings.

Q: What is the difference between personal and commercial truck insurance?

A: Personal truck insurance covers your truck for personal use — commuting, errands, recreation. Commercial truck insurance covers trucks used for business purposes, including hauling freight, running deliveries, or operating as a contractor. Most personal auto policies explicitly exclude commercial use, meaning claims arising from business use can be denied. For owner-operators running under their own authority, commercial truck insurance typically costs $900 to $2,500 per month depending on the truck type, cargo, operating radius, and driving history — a fundamentally different cost level from personal coverage.

Q: What coverage do I actually need for my pickup truck?

A: The right coverage depends on your truck’s value and your financial situation. If your truck is financed or leased, your lender requires full coverage — liability, collision, and comprehensive. If your truck is paid off and worth less than approximately $8,000, liability-only coverage may be financially rational. For trucks worth $15,000 or more, full coverage protects you against the financial loss of a total loss claim. Gap insurance is worth adding on new trucks where the loan balance exceeds the truck’s market value.

The Bottom Line

Truck insurance in 2026 costs $222 per month on average. The cheapest company charges $84. The cheapest truck insures for $176. The gap between what most people pay and what they could pay with the right information is significant — and it is entirely closeable.

The steps are not complicated. Get at least three quotes every time your policy renews. Consider the insurance cost before you buy your next truck. Check whether Auto-Owners operates in your state and get a quote if it does. If you qualify for USAA, use USAA. Bundle your home and truck with the same insurer. Ask for a discount review at every renewal. Keep a clean driving record — it is the single most powerful lever you have.

None of these steps require expertise. They require about two hours of attention per year. The return on those two hours, compounded over a five-year truck ownership period, is regularly $3,000 to $6,000. That is not a small number. That is a truck payment, a set of tires, or a vacation — paid for by doing nothing more complicated than making a phone call your insurance company is hoping you never make.

Make the call.

Editorial Note

This article was written and reviewed in March 2026. All insurance rate data is sourced from Insure.com (February 5, 2026), Insurify (February 1, 2026), MoneyGeek (February 9, 2026), The Zebra (January 15, 2026), and Logrock (February 10, 2026). All rates represent averages for comparison purposes — your actual rate will vary based on your driver profile, vehicle, location, and coverage selections. Insurance company availability varies by state. Always obtain quotes directly from insurance companies or licensed agents for accurate pricing specific to your situation. Commercial truck insurance rates cited are based on MoneyGeek’s 2025 analysis of $1 million CSL liability coverage.

0 Comments