Last Updated: April 11, 2026 | Read Time: 11 minutes

Yes, you can sell a car you are still paying off. But there are specific steps, specific legal requirements around the title, and a specific financial calculation you need to run before you list it anywhere. Here is everything you need to know — clearly, in the right order, with the real numbers and the real process.

Contents

At A Glance – Can You Sell A Car With A Loan In 2026

– Can you sell a financed car? Yes — but the loan must be paid off before the title transfers

– Who holds your title? Your lender holds it (or is listed as lienholder) until payoff

– Average auto loan balance in 2026: $23,792 (TransUnion)

– Percentage of private sellers who still owe money: 45%

– Positive Equity: Your car is worth more than you owe — you keep the difference

– Negative Equity: You owe more than your car is worth — you cover the gap

– Easiest selling method: Trade-in or dealer sale — dealer handles the lien and paperwork

– Most profitable method: Private sale — typically yields more money than a dealer or trade-in

– Escrow service fee: Typically 1.5% to 2% of the sale price (approximately $150 on a $10,000 sale)

– Payoff quote timing: Request a 10-day payoff amount — valid for 10 days from the date issued

– Title-holding states: Some states hold the title at the DMV until payoff — others issue it to the lender

– Credit impact: Generally minimal if the loan is paid in full — negative equity situations can have nuances

Sources: NerdWallet, LendingTree, Edmunds, Experian, Capital One Auto Navigator, CARFAX, U.S. News.

Overview – More People Are In Your Situation Than You Think

If you have a car loan and are thinking about selling the vehicle before it is paid off, the first thing to understand is that you are not doing something unusual. You are doing something that about half of all private car sellers do in any given year. According to Experian’s Auto Finance Report, 45 percent of private car sellers still owe money on their vehicle at the time of sale. Auto loans stretching up to 84 months and high vehicle prices mean that millions of Americans need or want to sell a car they have not yet finished paying for — every single year.

The second thing to understand is that selling a financed car is legal, common, and entirely manageable. It is not difficult. It does add steps to the process that a clean-title sale does not require. And it does have one non-negotiable rule that you cannot work around: the lender must be paid in full before the title can be transferred to the new owner.

Everything else in this guide is about how to navigate that one rule efficiently, legally, and in a way that protects both you and the buyer.

When you have a loan on a car, the lender is, in a sense, part owner of the vehicle. The lender’s name may be listed on the car title, or the lender may actually hold the title. This is to ensure you cannot sell the vehicle and transfer the title to the new owner without the lender getting its money. That arrangement — the lien — is what makes selling a financed car more involved than selling one you own outright. Understanding the lien and how to release it is the core skill this guide teaches.

Selling a financed car is often the first step in transitioning to a different vehicle — and before you buy the next one, understanding what insurance will cost on that vehicle is as important as understanding what the loan payment will be. Our complete breakdown of car insurance cost in the USA in 2026 gives you the full picture of what American drivers are paying and how to reduce it.

The process looks different depending on whether you have positive equity or negative equity in the car, and whether you are selling to a private buyer or to a dealership. This guide covers all four combinations clearly, with the exact steps for each.

Section 1 – The Fundamental Concept

What A Lien Is And Why It Controls The Sale

Before getting into the steps, it helps to understand the legal structure that makes selling a financed car more complicated than a simple cash sale.

When you take out an auto loan to buy a car, the lender does not simply give you money and trust you to pay it back. The lender places a lien on the vehicle — a legal claim on the asset that secures its interest in the loan. The lien is recorded on the title of the vehicle. In some states, called title-holding states, the lender physically holds the paper title until the loan is paid off. In other states, called non-title-holding states, the title is issued with the lender’s name listed as the lienholder, and the title itself is in the registered owner’s hands — but the lien is still on the record.

The lender will also place a lien on the vehicle to protect its investment. You will need to pay the loan in full before the lender will release the lien and title — allowing you to resell the vehicle to another party.

The practical consequence of the lien for a seller is straightforward: you cannot legally transfer a clear title to a buyer until the lien is released. You cannot release the lien until the loan is paid in full. The buyer cannot get a clean title — and therefore cannot legally register the car in their name — until the lien is gone. This is the sequence that every financed car sale must follow, and every method for selling a financed car is essentially a different mechanism for managing that sequence.

Section 2 – Step One: Know Your Numbers

Getting The Payoff Amount And The Car’s Market Value

Before you can make any decision about whether to sell, how to sell, or what to price the car at, you need two numbers. Without both of them, you are making financial decisions in the dark.

Before you get your car appraised for a payoff comparison, minor cosmetic repairs can meaningfully improve the appraisal value — scratches and paint damage reduce both dealer and Carvana offers by amounts that often exceed the repair cost. Our guide to how much it costs to paint a car in 2026 breaks down exactly what a single-panel touch-up to a full respray runs in today’s market

Getting Your Payoff Amount

The payoff amount is not the same as your current loan balance. Your current loan balance is how much principal you owe. The payoff amount is the total you would need to send to the lender today — or within a specific window — to satisfy the loan in full, including any accrued interest up to the payment date and any applicable fees.

Contact your lender to obtain the 10-day payoff amount, which is crucial for the following steps. There could be interest, penalties or other fees that you might not be aware of. The 10-day payoff quote is the standard format: it tells you exactly what you need to pay, and it is valid for 10 days from the date it is issued. If the sale takes longer than 10 days, request a new quote.

Most major lenders — including Ally, Capital One, Chase, and major credit unions — now have digital portals where you can access a payoff quote online without calling. Check your online dashboard before calling customer service. You can also attempt to negotiate a lower payoff amount with some lenders if they are flexible or offer to pay a lump sum payment that is less than the total payoff amount — though this is not common and works better in situations of financial hardship than standard sale scenarios.

One important fee to check: some lenders charge a prepayment penalty for paying off an auto loan early. These are not as common as they once were, but they exist. Confirm with your specific lender whether a prepayment penalty applies before assuming the payoff quote is your only cost.

Finding Your Car’s Current Market Value

The second number is your car’s current market value — what a buyer would actually pay for it today. You need this number from at least two independent sources, because values vary.

You can get a pretty good idea of its value at the Kelley Blue Book and Edmunds websites. Both sites provide forms you can use to enter the model and year, mileage, options packages, and other details about its configuration and condition. You can also get estimates from used car websites including used car buyers like Carvana and CarMax to make comparisons — these instant offer tools give you a guaranteed cash offer that serves as a useful floor for your private sale price.

Two important distinctions in these valuations: the trade-in value is lower than the private party sale value, because dealers need margin to resell the car at a profit. The private party value is what a person-to-person sale can realistically achieve. Generally, you will make more money if you sell your car privately — but the private sale process requires more work and time.

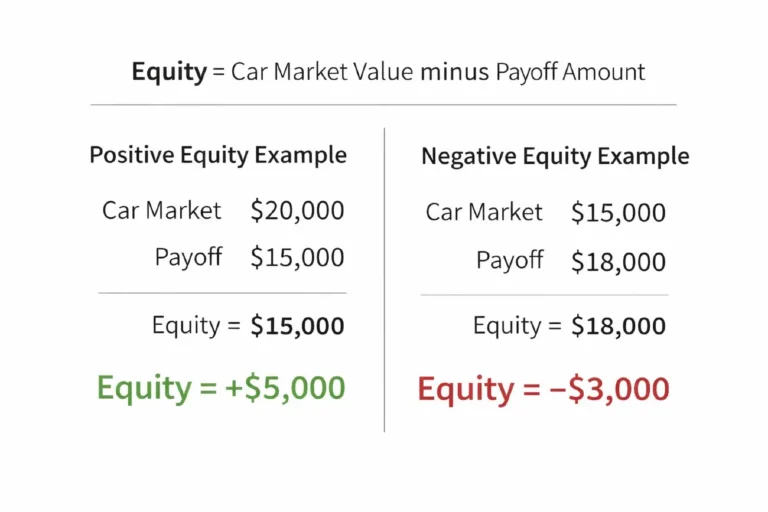

Calculating Your Equity Position

Equity is the number that determines which path you take from here:

Equity = Car’s Current Market Value — Payoff Amount

If the result is positive, you have positive equity. Your car is worth more than you owe. The sale proceeds will cover the loan and leave money for you.

If the result is negative, you have negative equity — also called being upside down on the loan. You owe more than the car is worth. The sale proceeds will not cover the full loan balance, and you will need to cover the difference from another source.

“Equity represents how much value is left over after paying off the loan and can be calculated by subtracting your payoff quote from your vehicle’s value,” according to Matt Dundas, senior director of finance with Carvana. You can sell a car with positive or negative equity, but the process will look a little different.

Section 3 – Option One: Selling To A Dealer Or Trading

The Simplest Method — Less Money, Less Headache

The easiest way to sell a car on which you still owe money is to trade it in or sell it to a dealer, because they will handle the paperwork and make sure the lienholder is paid. Once it is, the lien on the car’s title can be removed and the title can be transferred to the new owner.

When you sell or trade in your car to a dealership, they typically handle the title transfer as part of the process. The dealer will appraise the car, call the lender and get a payoff amount. If there is equity, you can use all, some, or none of the equity as a down payment on the vehicle you are buying. Typically, the equity is applied to the out-the-door price and an unpaid balance is due.

In negative equity situations, the dealer can help you roll in your outstanding loan balance to your new car loan. This is where caution is warranted. Rolling negative equity into a new loan means you are immediately upside down on the new vehicle before you have even driven it off the lot. You are paying interest on a balance that represents a loss from the previous car, not value in the new one. This is the situation that creates the cycle of perpetually being upside down on a vehicle — every trade-in rolls negative equity forward, compounding the problem.

A dealer trade-in also has a specific tax advantage worth knowing. In many states, the value of your trade-in can be subtracted from the price of your next car when calculating sales taxes due, which can add up to hundreds or thousands of dollars in savings. If you are buying a new vehicle at the same time as selling, the dealer’s trade-in route sometimes saves enough in taxes to partially offset the lower price you receive compared to a private sale.

The process at a dealer is straightforward: they appraise your car, confirm the payoff amount with your lender, complete the paperwork, and issue payment directly to the lender. You receive any equity above the payoff amount as a credit toward your next purchase or as a check. The entire process typically completes in one visit.

Selling directly to platforms like Carvana or CarMax follows a similar logic — they handle the lender payoff and manage the title transfer. You will receive an instant offer, sell the car, and the platform pays off the loan directly. This is marginally more than a standard dealer trade-in for many vehicles and significantly more convenient than a full private sale.

One of the most common reasons a driver sells a financed car is because life circumstances have changed — a teenager has become a new driver and the family needs a different vehicle. If that is your situation, our guide to the best first cars for teenagers in 2026 covers every vehicle in the segment that combines safety, insurance affordability, and appropriate performance for a new driver.

Section 4 – Option Two: Selling To A Private Buyer With Positive Equity

More Work, More Money — Here Is Exactly How To Do It

Selling a financed car with positive equity to a private buyer is the most profitable route and also the most involved. It is entirely doable — millions of people complete this transaction every year. The key is communication: with your lender, with your buyer, and about the timeline and process.

You do not need to put this loan information in your listing to sell the car. But once you feel you have a serious buyer, explain the situation before arranging a test drive. Tell them that you have talked with your lender and know the exact steps required.

This transparency is important for two reasons. First, it prevents wasted time — a buyer who discovers mid-process that there is a lien and does not understand it may walk away unnecessarily. Second, it builds trust. When a seller explains the process clearly and confidently, it signals that they are organized, honest, and that the transaction will be handled correctly.

There are two common mechanisms for completing a private sale with a financed car:

Method A — Two Checks At The Lender’s Branch

This is the most straightforward method if you have a local branch lender such as a bank or credit union. The buyer meets you at the lender’s office. One check goes directly to the lender for the exact payoff amount. A second check goes to you for the equity — the difference between the sale price and the payoff amount.

The buyer hands the lender a check, and the lender turns the vehicle’s title over to the buyer. The buyer then gives you the remaining amount. The lender processes the payoff immediately, releases the lien, and either hands over the title or initiates the title transfer to the buyer directly. This method gives the buyer immediate confidence — they are handing money to a financial institution and receiving the title in the same transaction.

Method B — Buyer Pays The Full Amount To The Lender, Lender Sends You Your Equity

In this version, the buyer writes a single check for the full purchase price to the lender. The lender applies the payoff amount to close the loan, releases the lien, and sends you a check for the equity portion. The title is transferred to the buyer.

This method works well when the buyer prefers to make a single payment rather than writing two checks. It requires trust in the lender’s process but has the advantage of simplicity.

Using An Escrow Service

For private sales where neither party wants to meet at a bank — particularly when buyer and seller are in different cities or when the transaction involves an online platform — an escrow service is an excellent solution.

An escrow service will assume the responsibility of overseeing your loan payments, and it will handle the paperwork involved in the sale, dealing directly with your lienholder to facilitate a swift title transfer. Once it has used the buyer’s funds to pay off your loan, the escrow service will release whatever is left to you.

The drawback of using an escrow service is that it is not free, but the fee is typically quite small — often roughly 1.5 percent to 2 percent of the vehicle’s sale price, or $150 on a $10,000 transaction. For transactions involving larger amounts or significant geographic distance between buyer and seller, the escrow fee is a reasonable cost for the security and simplicity it provides.

Section 5 – Option Three: Selling With Negative Equity

The Harder Conversation — But Not The Impossible One

Negative equity — being upside down on a car loan — is more common than most people realize. Long loan terms, rapid depreciation in the early years of vehicle ownership, and high vehicle prices all contribute to situations where a driver owes more on a car than it is currently worth. You owe more than your car’s current market value.

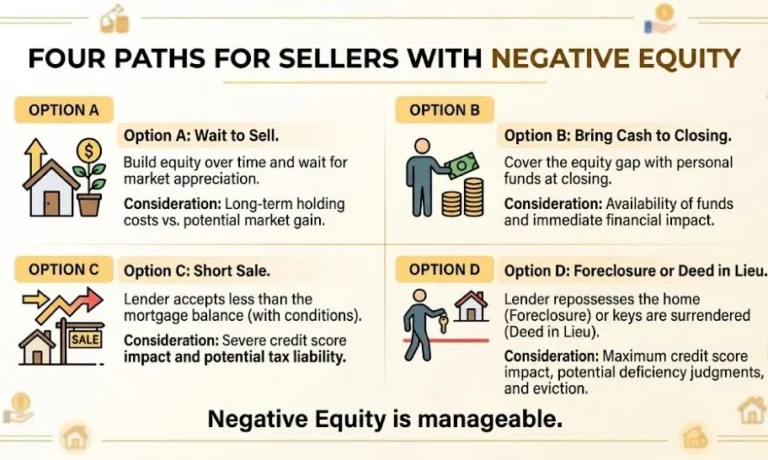

If you need to sell a car with negative equity, your options are:

Option A — Pay The Difference Out Of Pocket

The cleanest solution. If the payoff amount is $18,000 and the car is worth $15,000, you cover the $3,000 gap yourself. This eliminates the debt immediately, frees you from the ongoing car payment, and leaves no lingering obligation. If you have savings that can absorb the difference, this is often the correct financial decision — particularly if the monthly payment is a significant burden or if you need a different vehicle for changed circumstances.

Option B — Roll The Negative Equity Into A New Loan

The most common dealer-facilitated approach. The negative equity from your current vehicle is added to the financing on your next vehicle. You owe $3,000 more than the new car is worth from day one. This is a financially consequential decision that should be made with clear understanding of the total interest cost.

Rolling $3,000 negative equity into a new loan at 7.5 percent adds approximately $900 in interest over a five-year loan term — on top of the negative equity itself. Over successive trade-in cycles, this compounds significantly. It is the right choice in some circumstances — when the new vehicle purchase is truly necessary and the monthly payment math works — but it should be treated as a calculated cost, not a neutral transaction.

Option C — Take A Personal Loan To Cover The Gap

If you have good credit, taking an unsecured personal loan to cover the negative equity balance before the sale can simplify the process. With an unsecured personal loan, the lender will not be placed on the title. The title will come to you and the car will be yours alone to sell, simplifying the process. But rates on unsecured personal loans, even if your credit is excellent, will be higher than most auto loans — pay it off as soon as you have the buyer’s check banked.

This approach is useful when you want to sell privately — a cleaner title situation is more reassuring to private buyers than coordinating a sale through a lender with an outstanding balance. Get the personal loan, pay off the auto loan, receive the clear title, sell the car privately, and then immediately pay off the personal loan from the sale proceeds.

Option D — Wait And Continue Paying

If negative equity is not severe and the financial pressure to sell is not urgent, continuing to make payments while building equity through principal reduction is a valid option. Depreciation curves vary by vehicle — trucks and certain SUVs hold their value better than sedans in many markets — and the gap between what you owe and what the car is worth may narrow meaningfully within six to twelve months of continued payments.

Section 6 – The Title Transfer Process

State-By-State Differences And What The Buyer Needs

The title transfer process for a financed car sale varies by state in ways that can significantly affect the timeline and logistics of the transaction.

Title-Holding States

In non-title-holding states, titles on a financed vehicle are held by the lender until the loan is paid in full, after which the title is reissued in the owner’s name. When you sell a car before it is paid off in one of these states, you must arrange for the lender to transfer title to the new owner. Contact the lender or your state Department of Motor Vehicles for details on this process.

States that operate as non-title-holding states include Kentucky, Maryland, Michigan, Minnesota, Missouri, Montana, New York, and Oklahoma, among others. In these states, the physical title is at the lender’s office and the payoff must be completed before you can provide it to the buyer.

Non-Title-Holding States

In title-holding states — including California, Texas, Florida, and most of the remaining states — the registered owner possesses the physical title, but the lender’s name appears on it as the lienholder. When the loan is paid off, the lender signs off on the title (or issues a separate lien release document), which you then provide to the buyer.

In practice, for a private sale in a title-holding state, the sequence is: payoff completes, lender signs the title or provides a lien release, title and lien release go to the buyer, buyer takes both documents to the DMV to register the vehicle and get a new title in their name.

The buyer can then take the title to their local Department of Motor Vehicles office to register the car in their name.

What To Do After The Sale

Once the sale is complete, get written documentation from your lender that the loan has been paid in full and the lien has been satisfied. This protects you from any future dispute about the loan status and provides proof of payoff if needed for your own records or for the buyer’s records.

Follow up afterward and make sure the original loan gets paid in full. With online lender portals, you can confirm this directly. If a lender or credit bureau does not update your loan balance to zero within 30 to 60 days, you may want to dispute the error with the appropriate credit reporting agency.

If a dispute with the credit reporting agency does not resolve a loan balance that has not been updated to zero after payoff, submit a complaint to the Consumer Financial Protection Bureau complaint portal — the CFPB has enforcement authority over financial institutions and their obligation to report accurate account information.

Section 7 – How Selling A Financed Car Affects Your Credit

The Credit Impact Is Often Minimal — But There Are Nuances

Selling a car you are still paying off typically does not have a major impact on your credit, but it can influence your credit profile in a few ways worth understanding before the sale.

Positive Equity Sale — Minimal Credit Impact

If you sell the car with positive equity and the loan is paid in full from the proceeds, the loan account closes. A closed account in good standing remains on your credit report for up to 10 years and continues to contribute positively to your credit history length.

The one nuance: if you have positive equity in the car and do not take out a new car loan after the sale, closure of your car loan account could reduce your credit mix — a factor responsible for about 10 percent of your FICO score. This should not be a big concern, but you may notice a small temporary drop in your scores. It typically recovers as the rest of your credit profile continues to demonstrate responsible behavior.

Negative Equity Sale — Depends On How You Handle The Gap

If you have negative equity in the vehicle when you sell it and continue making regular payments until the loan is paid in full — covering the shortfall over time rather than immediately — those payments will factor into your debt-to-income ratio during the period you are still paying. This can affect your ability to qualify for a new vehicle loan immediately after the sale.

If you pay the gap immediately — in cash, with a personal loan, or by covering the dealer’s rollover — the loan closes and the credit impact is the same as a positive equity sale.

The worst credit outcome in a financed car sale scenario is defaulting on the remaining balance after a sale — failing to pay the gap between the sale proceeds and the payoff amount. This can result in a collection account, which has severe and lasting credit consequences. Always ensure the gap is covered before completing the sale.

Section 8 – Special Situations

Loan Assumption, Online Platforms, And Tax Considerations

Can A Buyer Assume Your Loan?

Loan assumption — where a buyer takes over the remaining payments on your existing loan rather than paying you and the lender separately — is theoretically possible but practically rare. Loan assumption requires a buyer with typically a 700 or higher FICO score who qualifies with your specific lender under their specific terms. Most major lenders do not advertise or facilitate personal auto loan assumptions, and the process is sufficiently complex that most transactions do not go this route.

It can be done, but it can also be messy. As the seller, you will have to find someone who not only wants to buy your car, but who also qualifies with your lender to take over your loan. If the buyer defaults after assumption, your credit may be affected depending on how the lender structures the transition. This is a path to discuss specifically with your lender if it interests you — do not assume it is available without confirming.

Selling Through Online Platforms — Carvana, CarMax, Vroom

The growth of online car-buying platforms has made selling a financed car significantly simpler for many owners. Platforms like Carvana, CarMax, and Vroom all accept financed vehicles. You enter your information online, receive an offer, provide the payoff amount, and the platform pays the lender directly.

If the offer exceeds the payoff amount, you receive the difference. If the payoff amount exceeds the offer — negative equity — you will be asked to pay the difference before the sale completes. The process is entirely digital for most steps and eliminates the complexity of coordinating a private sale with a lienholder.

The trade-off is that online platform offers are typically lower than private party sale values — often comparable to dealer offers. You are paying for convenience and simplicity.

Tax Implications

Before you sell a car with a loan, make sure you are aware of the tax implications so you do not get hit with a costly surprise. Depending on how your loan was set up, you may have paid taxes upfront, or more likely they have been rolled into your monthly payment. Confirm with your lender and your state’s Department of Motor Vehicles whether you will owe any taxes once the car is titled in your name.

In most states, selling a personal use vehicle at a loss — which is common when selling used cars — does not create a taxable gain. However, if you sold a vehicle that was used for business and depreciated for tax purposes, the sale may trigger a taxable event. Consult your tax preparer if your vehicle has any business use history before completing the sale.

Once you have completed the sale and are ready to insure your next vehicle, the choice of insurer matters as much as the choice of car — our guide to the cheapest car insurance companies in 2026 ranks every major national and regional insurer by actual rate so you enter the market with real numbers.

Section 9 – Common Mistakes To Avoid

What Goes Wrong And How To Prevent It

Mistake 1 — Agreeing To A Price Before Knowing Your Payoff Amount

This is the single most common mistake in financed car sales. A seller agrees to a price with a buyer and then discovers the payoff amount is higher than expected — leaving them either short on the deal or needing to renegotiate. Always get the 10-day payoff amount from your lender before you set your asking price or accept any offer.

Mistake 2 — Not Disclosing The Loan To The Buyer Early Enough

Waiting until the buyer is ready to complete the transaction to reveal the loan adds complexity at the worst possible moment. Be transparent with serious buyers early in the process. Explain that there is a loan, that you know exactly what the payoff amount is, and that you know exactly how the title transfer will work. Buyers who understand the process are far less likely to back out than buyers who encounter it as a surprise.

Mistake 3 — Using The Buyer’s Money Without Paying Off The Loan

This is the scenario that can cross into fraud. A seller receives the full payment from a buyer, fails to pay off the loan with the proceeds, and the buyer is left with a car they cannot title in their name. Always complete the payoff before or simultaneously with transferring the car. Escrow services exist specifically to prevent this from happening accidentally or intentionally.

Mistake 4 — Not Getting Written Payoff Confirmation

After the loan is paid off, get written documentation from your lender confirming the payoff and lien release. Do not assume because you made the payment that the record is updated. Follow up in writing and keep the documentation permanently.

Mistake 5 — Rolling Negative Equity Forward Without Understanding The Full Cost

Rolling negative equity into a new loan feels like a neutral transaction — the number disappears from your current vehicle and reappears on the new one. But you are paying interest on that balance for the entire life of the new loan. Calculate the total cost of rolling the negative equity before agreeing to it.

FAQ

Q: Can you sell a car if you still owe money on it?

A: Yes. You can sell a car even if you still have an outstanding loan on it. However, the loan must be paid off in full before the title can be transferred to the new owner. The lender holds a lien on the vehicle that prevents title transfer until the payoff is complete. The sale process involves coordinating with your lender, obtaining a payoff quote, and arranging for the loan to be satisfied — either from the sale proceeds, out of pocket, or through dealer facilitation.

Q: What is the difference between positive and negative equity?

A: Positive equity means your car’s current market value is higher than your loan payoff amount. If your car is worth $20,000 and your payoff is $15,000, you have $5,000 in positive equity — the sale proceeds cover the loan and you keep the rest. Negative equity means you owe more than the car is worth. If your car is worth $15,000 and your payoff is $18,000, you have $3,000 in negative equity — the sale proceeds do not cover the full loan and you must cover the $3,000 gap from another source.

Q: How do you get your payoff amount?

A: Contact your lender — by phone, by logging into your online account portal, or by visiting a local branch — and request a 10-day payoff quote. The payoff quote will include the remaining principal balance, accrued interest through the payment date, and any applicable fees. The quote is valid for 10 days. If your sale takes longer than 10 days, request a new quote. Most major lenders provide this online without requiring a phone call.

Q: What is the easiest way to sell a financed car?

A: The easiest way to sell a financed car is to trade it in or sell it to a dealership. The dealer handles the payoff process, communicates with the lender, manages the title transfer, and completes all the paperwork. You lose some sale value compared to a private sale, but the simplicity is significant — the entire process typically completes in a single dealership visit. Online platforms like Carvana and CarMax offer a comparable level of simplicity for sellers who do not want to visit a dealership.

Q: Can you sell a financed car to a private buyer?

A: Yes. Selling a financed car to a private buyer is more involved than a dealer sale but typically more profitable. The most common methods are: meeting the buyer at the lender’s branch where the buyer pays the lender directly and you receive any equity; using an escrow service that manages the payoff and title transfer; or paying off the loan before listing the car, which gives you a clean title and simplifies the private sale significantly.

Q: What happens if I still owe more than the car is worth?

A: If you owe more than the car is worth — negative equity — you have several options. You can pay the difference out of pocket to complete the sale. You can roll the negative equity into a new vehicle loan if you are purchasing another car. You can take an unsecured personal loan to cover the gap, complete the sale, and then immediately repay the personal loan from the proceeds. Or you can continue making payments until the loan balance falls to or below the car’s value before selling. The dealer trade-in route is the most common path for negative equity situations because the dealer facilitates the process.

Q: Will selling a financed car hurt my credit?

A: Generally, no. Selling a financed car and paying off the loan in full is a positive credit event — the loan closes in good standing. You may see a small, temporary dip in your credit score if the closed account reduces your credit mix, but this is minor and typically recovers quickly. The one scenario that significantly hurts credit is failing to cover a negative equity gap after the sale — if the remaining loan balance is not paid, it can go to collections and have a severe credit impact.

Q: Can a buyer take over my car loan?

A: Loan assumption — where a buyer formally takes over the responsibility for your loan — is possible but rare. It requires the buyer to qualify with your specific lender at that lender’s terms and credit requirements, typically needing a 700 or higher FICO score. Most major lenders do not readily offer or advertise personal auto loan assumption. Contact your specific lender to confirm whether loan assumption is available before presenting it to a buyer as an option.

The Bottom Line

Selling a car with a loan is not complicated. It is extra steps around one core requirement: the lender must be paid before the title moves. Once you accept that requirement as the framework, every other decision — dealer or private, escrow or branch meeting, cover the gap or roll it forward — is just a question of which method best fits your situation, your timeline, and your financial position.

Know your payoff amount. Know your car’s market value. Know whether you have positive or negative equity. Choose the selling method that fits those numbers. Be transparent with your buyer. Get written payoff confirmation when it is done.

The 45 percent of sellers who complete this process every year are not financial experts or car industry insiders. They are people who needed to sell a car they had not finished paying for, who figured out the steps, and who completed the transaction legally and without incident. The steps in this guide are exactly what they followed. There is no reason your situation should be any different.

Editorial Note

This article was written and reviewed in April 2026. All data on average loan balances and percentage of sellers with outstanding loans is sourced from Experian’s Auto Finance Report and TransUnion’s auto lending data. Process guidance is sourced from NerdWallet , LendingTree, Edmunds, CARFAX, Capital One Auto Navigator, Experian, Rocket Loans, and U.S. News. Expert quotes are attributed to their original sources including Grant Feek of Cox Automotive and Matt Dundas of Carvana as published in U.S. News. Tax and credit guidance is general educational information and should not be treated as legal or financial advice for any specific situation. Consult a financial professional or tax advisor for guidance specific to your circumstances.

0 Comments