Last Updated: April 3, 2026 | Read Time: 12 minutes

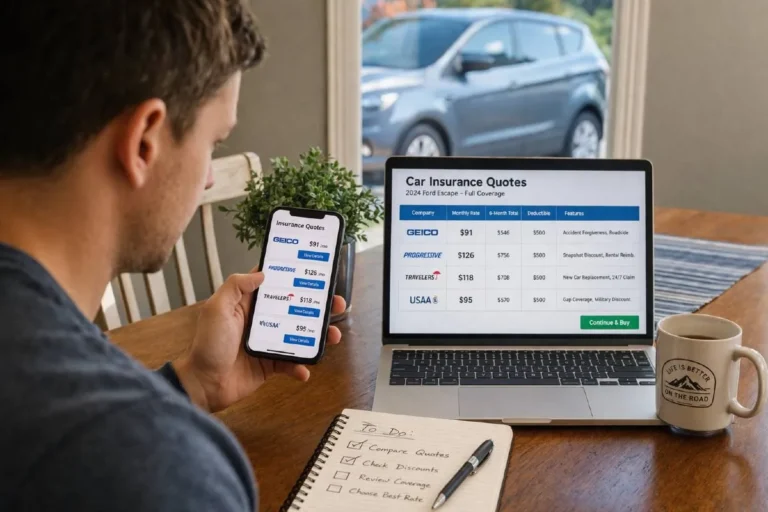

Travelers is charging $139 a month for full coverage. GEICO is charging $41 a month for liability. USAA is at $130 for those who qualify. The national average is $218. Here is exactly who charges what, who is cheapest for your specific situation, and how to pay even less than the cheapest published rate.

At A Glance – Cheapest Car Insurance Companies 2026

Full Coverage — Cheapest Companies:

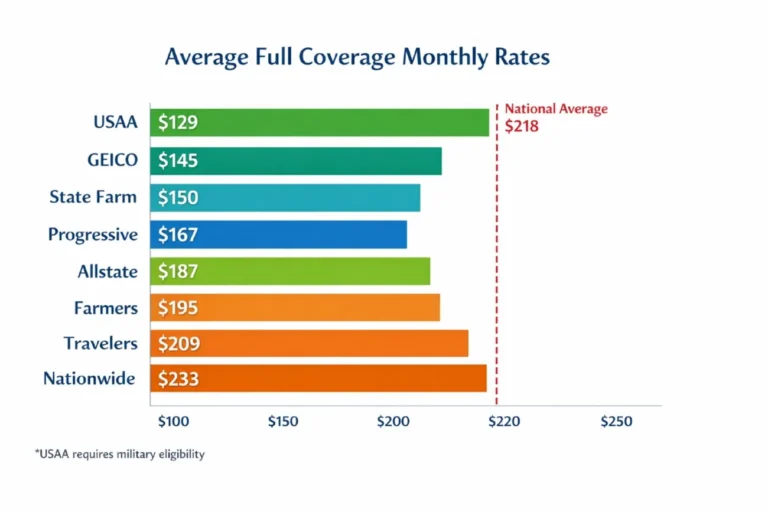

– USAA: $1,542/year — $129/month (military/veterans only)

– Travelers: $1,665/year — $139/month (NerdWallet March 2026)

– Erie Insurance: $1,908/year — $159/month (regional — not available all states)

– Auto-Owners: $2,052/year — $171/month (regional — 26 states)

– GEICO: $2,052/year — $171/month

– State Farm: $2,123/year — $177/month

– Progressive: $2,057/year — $171/month

Liability Only — Cheapest Companies:

– USAA: $412/year — $34/month

– GEICO: $494/year — $41/month

– Erie: $445/year — $37/month

– Auto-Owners: $540/year — $45/month

– Progressive: $619/year — $52/month

– National Average Full Coverage: $2,611/year — $218/month

– National Average Liability Only: $1,407/year — $117/month

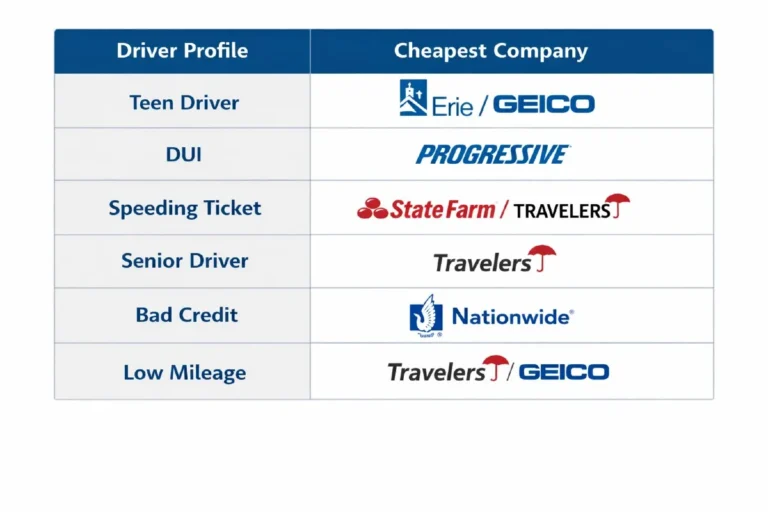

– Best for Teens: Erie, USAA, GEICO

– Best for DUI: Progressive ($3,625/year)

– Best for Speeding Ticket: State Farm and GEICO ($56/month minimum)

– Best for Bad Credit: Nationwide ($299/month full coverage)

– Best for Seniors: Travelers ($173/month full coverage)

Sources: NerdWallet, U.S. News March, MoneyGeek, Insurance.com December, CarInsurance.com

Overview – The Number That Should Make Every Driver Uncomfortable

The national average for full coverage car insurance in 2026 is $2,611 per year — $218 every month. If you are paying close to that number, there is a very good chance you are overpaying. Not because your needs are unusual or your profile is exceptional, but because the car insurance market has a specific characteristic that almost every other major consumer financial market does not: the price difference between the cheapest and most expensive option for the same coverage from the same starting profile can exceed 100 percent.

Travelers charges the average 40-year-old driver with a clean record $133 a month for full coverage. A comparable policy from some national carriers costs $250 or more. The coverage is equivalent. The financial protection is identical. The difference is entirely in which company you chose — and most people chose based on a TV commercial, a renewal notice, or the sticker price they were quoted three years ago and have been paying ever since.

Travelers is the cheapest large auto insurance company in the nation for full coverage, with an average rate of $139 a month and $1,665 a year, according to NerdWallet’s March 2026 analysis. GEICO is the cheapest large auto insurance company for liability coverage, with an average rate of $41 a month and $494 a year.

But here is the critical complexity in the cheapest car insurance conversation: the cheapest company for a 40-year-old driver with a clean record in Ohio is not the cheapest company for a 25-year-old driver with a speeding ticket in Florida. The cheapest company for someone with excellent credit is not the cheapest for someone with a difficult credit history. The car insurance market does not have a single cheapest option. It has a cheapest option for every combination of driver profile, location, vehicle, and coverage level — and finding yours requires understanding how these profiles interact with each company’s pricing models.

The scale of the American car insurance market — and the factors driving recent premium increases — is documented comprehensively by the Insurance Information Institute car insurance facts page, the primary industry research organization for insurance data in the United States.

This guide provides all of it — the real 2026 rates, the cheapest company for every major driver category, and nine strategies that produce savings beyond even the cheapest published rate.

Section 1 — The Cheapest Companies Ranked

Every Major Insurer, Real Rates, Honest Assessment

USAA — Cheapest Overall: $129/Month Full Coverage

USAA has the cheapest average annual rate for minimum coverage ($412) and full coverage ($1,542). If you don’t qualify for USAA, GEICO has the second-lowest for minimum coverage, and Travelers has the second-lowest for full coverage.

USAA is the benchmark against which every other car insurance company competes — and consistently loses. An average of $129 per month for full coverage is $89 per month less than the national average. Over a standard three-year car ownership period, that difference amounts to $3,204 — a significant sum that qualified drivers who are not using USAA are leaving on the table.

The qualification requirement is non-negotiable: active duty military, veterans, National Guard members, reservists, and the immediate family members of any qualifying individual. USAA eligibility flows downstream — spouses and children of members qualify; parents or in-laws do not. If you qualify and are not currently insured with USAA, getting a quote from them before your next renewal is not optional advice. It is the highest-return action available to you.

USAA also consistently leads in customer satisfaction. It earned the second-highest rating in the J.D. Power 2025 U.S. Auto Claims Satisfaction Study and holds an AM Best financial strength rating of A++ — the highest available rating for an insurer’s ability to pay claims. Cheap and reliable is a combination that most industries struggle to deliver simultaneously. USAA consistently does.

Travelers — Cheapest National Insurer For Full Coverage: $139/Month

For drivers who do not qualify for USAA, Travelers is the next-cheapest company, according to research from both U.S. News and NerdWallet published in March 2026. At $139 per month for full coverage — $1,665 annually — Travelers is $79 per month below the national average and a genuinely competitive option for virtually every driver profile.

Travelers is also one of the most consistently strong performers across specific driver categories. Travelers is the cheapest for 40-year-old drivers, with an average rate of $133 a month. Travelers also charges the lowest full coverage rate after a speeding ticket at $129 monthly — significantly below what most competitors charge for the same situation. For senior drivers, Travelers averages $173 per month for full coverage — among the cheapest in that demographic.

Travelers holds an AM Best financial strength rating of A++, matching USAA’s superior rating. Their IntelliDrive telematics program offers additional discounts of up to 30 percent for drivers who demonstrate safe driving behavior during a monitoring period — making the effective rate for safe drivers potentially well below even the $139 monthly average.

Erie Insurance — Cheapest Regional Company: $159/Month Full Coverage

Erie Insurance offers the most affordable auto insurance rates on average, with full coverage averaging $159 per month and liability-only coverage costing $37 per month. Among regional insurers, Erie consistently outperforms every national carrier on both price and customer satisfaction.

The significant caveat: Erie operates in only 12 states — Illinois, Indiana, Kentucky, Maryland, New York, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, and Wisconsin, plus Washington D.C. If you live in one of these states and have not gotten an Erie quote, you are very likely overpaying.

Erie’s Rate Lock program — which guarantees your rate will not increase at renewal unless you change your policy, add a driver, or move to a different address — is one of the most genuinely valuable features in personal auto insurance. Rate creep at renewal is one of the most common ways car insurance costs increase for long-term policyholders. Erie’s Rate Lock eliminates it as a concern.

For teen drivers specifically, our research shows that Erie and USAA are the most affordable for teenage drivers. Erie’s average for teen coverage is among the lowest available from any carrier nationally.

Auto-Owners Insurance — Cheapest In 26 States: $171/Month Full Coverage

Auto-Owners offers very competitive car insurance at $171 per month for full coverage — essentially matched with GEICO at the same average rate but typically more competitive in the specific states where it operates. Auto-Owners is available in 26 states and consistently ranks among the top two or three cheapest options in most of its markets.

Auto-Owners’ customer satisfaction ratings are consistently excellent. Their complaint ratio with the NAIC is well below the industry average, and their claims handling reputation is among the best of any carrier operating at their price point. Where Auto-Owners is available and you have not gotten a quote, you are missing one of the most competitive options in your market.

GEICO — Cheapest National Carrier For Liability: $41/Month

GEICO is the cheapest large auto insurance company in the nation for liability coverage, with an average rate of $41 a month and $494 a year. For full coverage, GEICO averages $171 per month — competitive with Auto-Owners and Progressive at similar price points.

GEICO’s strongest competitive position is liability-only coverage, minimum coverage policies, and drivers with clean records in standard risk profiles. GEICO offers the lowest price on state minimum car insurance in more states than any other carrier. If your primary concern is meeting your state’s minimum liability requirement at the lowest possible cost, GEICO is typically the first number to beat.

GEICO also offers specific structured discounts that benefit targeted groups: military members and federal employees receive 12 to 15 percent discounts, the multi-vehicle discount runs up to 25 percent, and low-mileage discounts of 5 to 15 percent apply to drivers logging under 7,500 miles annually. GEICO’s mobile app and online claims process are among the most seamless in the industry.

One important note: GEICO increases its rates more aggressively than most competitors after certain violations. After a DUI, GEICO’s rates jump by 155 percent — one of the highest penalty increases among major national carriers. For drivers with clean records, GEICO is excellent value. For drivers with recent violations, it may not be.

Progressive — $171/Month Full Coverage And Best For Violations

Progressive’s average full coverage rate of $171 per month puts it in competitive range with GEICO and Auto-Owners. Progressive is $2,057 per year, $171 per month for full coverage — essentially tied with GEICO on average rates. Where Progressive differentiates is in its pricing flexibility for non-standard risk profiles.

Progressive offers the cheapest car insurance for drivers with a DUI, with average rates of $302 per month — significantly lower than GEICO’s post-DUI rate and competitive with any national carrier for that risk profile. Progressive is also the cheapest large auto insurance company for 20-year-old drivers at $306 per month — the best rate available from any major national carrier for young drivers.

Progressive’s Snapshot telematics program offers among the most generous safe-driver discounts available — drivers who demonstrate consistently smooth driving behavior during the monitoring period can reduce their rate by 20 to 30 percent from the base quote. For young drivers who are genuinely careful, Snapshot represents a meaningful path to lower rates that a standard quote does not capture.

Progressive holds an AM Best financial strength rating of A+ (Superior) — one step below USAA and Travelers’ A++ but still an indicator of strong financial health and claims-paying ability. Progressive’s 19 available discounts exceed most competitors’ discount catalogs.

State Farm — $177/Month Full Coverage And Best After Speeding Ticket

State Farm averages $177 per month for full coverage — slightly above GEICO and Progressive but with strong customer satisfaction ratings and a nationwide network of local agents that appeals to drivers who prefer in-person service. State Farm and GEICO both have the cheapest car insurance after a speeding ticket at $56 monthly for minimum coverage, 25 percent and 24 percent below the national median respectively.

State Farm’s bundling discounts — 10 to 25 percent off for combining home and auto insurance — are among the strongest in the industry. For homeowners who are currently insuring their home and car with different companies, a State Farm bundling quote frequently produces total combined savings that make it the economically rational choice even if its standalone auto rate is not the absolute cheapest.

State Farm’s Drive Safe and Save telematics program offers up to 30 percent discount for safe driving behavior, and the Steer Clear program provides specific discounts for drivers under 25 who complete a driver training module through the State Farm app.

Nationwide — $233/Month Full Coverage And Best For Bad Credit

Nationwide averages $233 per month for full coverage — above Travelers, GEICO, and Progressive at national average rates. Where Nationwide earns its position in this guide is its specific strength for drivers with poor credit.

Drivers with bad credit can find affordable car insurance with Nationwide, with rates averaging $299 per month for full coverage. In most states, insurers use a credit-based insurance score as a pricing factor — and poor credit can raise car insurance premiums by 60 to 80 percent above the rates a good-credit driver would pay. Nationwide’s treatment of credit-impaired drivers is more favorable than most competitors, making it the top recommendation for this specific profile.

Nationwide also offers the SmartRide telematics program and strong multi-policy bundling discounts. Its coverage options are comprehensive and include vanishing deductible programs that reduce your deductible by $100 for every claim-free year.

Section 2 – Cheapest By Driver Profile

The Right Company For Your Specific Situation

Cheapest For Teen Drivers (16–19)

Finding cheap car insurance for young drivers is genuinely difficult. A 20-year-old driver would pay $306 a month, on average, for the same coverage that costs a 35-year-old driver $139. The rate difference reflects statistical claim frequency, not anything specific about any individual young driver — but it is real and significant.

The cheapest car insurance for a 17-year-old is from Travelers, USAA, and GEICO. These companies charge the average 17-year-old driver as little as $1,325 per year for minimum coverage, while the average car insurance company charges 17-year-olds around $2,339 per year. GEICO offers the most affordable car insurance for male teen drivers aged 16 to 19, with full coverage costing an average of $6,441 annually — high in absolute terms but among the lowest available for this demographic.

The most effective cost-reduction strategy for teen drivers: add them to the family policy rather than buying a separate policy. Staying on the family policy until the young driver has more experience is typically cheaper than a standalone policy and is the approach most major carriers encourage. The good student discount — typically 10 to 15 percent for maintaining a B average or higher — is one of the most straightforward savings available for teen drivers.

Cheapest For Drivers With A DUI

A DUI conviction is one of the most expensive incidents a driving record can carry. Car insurance premiums will increase anywhere from 35 percent to 155 percent depending on the insurer. Progressive is the cheapest company after a DUI, with an average annual cost of $3,625. GEICO increases its rates by 155 percent — the highest penalty among national carriers — making it one of the worst choices for a post-DUI policy.

Progressive, State Farm, and Travelers are the recommended starting points for drivers seeking coverage after a DUI. Shopping around after any violation can save $400 to $900 yearly. An SR-22 requirement — which many states mandate after a DUI — adds a filing fee and raises base rates further, but Progressive and State Farm both handle SR-22 filings efficiently.

Cheapest For Drivers With A Speeding Ticket

A speeding ticket raises rates by 19 to 64 percent depending on the insurer. State Farm and GEICO both have the cheapest car insurance after a speeding ticket at $56 monthly for minimum coverage, 25 percent and 24 percent below the national median respectively. Travelers has the lowest full coverage rate at $129 monthly after a speeding ticket.

Speeding tickets typically stay on your record and affect rates for three to five years depending on state. Shopping your policy to these carriers immediately after a ticket — rather than staying with your current insurer and absorbing their penalty rate — can produce meaningful savings during the years the ticket affects your profile.

Cheapest For Senior Drivers (65+)

Travelers offers the most affordable car insurance for senior drivers among the insurance companies in research from both Insurance.com and U.S. News, with full coverage averaging $173 per month. For liability only, GEICO and USAA are among the cheapest for drivers aged 65, charging as little as $461 per year for minimum coverage.

Rates start rising again around age 70 as accident rates increase. If you drive fewer than 7,500 miles yearly — common for retirees — low-mileage discounts from GEICO or Progressive can offset some of that increase. Defensive driving course discounts are also available at most carriers for senior drivers who complete an approved course.

Cheapest For Drivers With Bad Credit

Your credit score will often factor into your auto insurance rates — people with no credit pay 67 percent more than people with excellent credit on average. In states where credit-based insurance scoring is permitted, improving your credit score is the highest-leverage long-term strategy for reducing your premium.

For drivers with poor credit in 2026, Nationwide averages $299 per month for full coverage — significantly below what most national carriers charge for the same driver profile. Regional carriers in specific markets can sometimes be competitive for credit-impaired drivers as well. Always get at least three quotes when shopping with a challenging credit profile, as pricing variation across carriers for this segment is wider than for standard profiles.

Cheapest For Low-Mileage Drivers

Drivers who log fewer than 7,500 miles yearly qualify for low-mileage discounts at GEICO, State Farm and Progressive. GEICO’s low-mileage discount runs 5 percent to 15 percent. Progressive’s Snapshot program can reduce rates further if your driving habits are consistently low-risk.

If you log less than 12,000 miles a year on your car, you can get car insurance for only $160 a month from Travelers. Pay-per-mile insurance programs — offered by Metromile and as an option through some major carriers — can reduce costs further for drivers who use their car infrequently. For drivers logging under 5,000 miles annually, pay-per-mile programs can produce the lowest available effective rate from any source.

Section 3 – Full Coverage vs Liability Only

Which Coverage Level You Actually Need And What It Costs

One of the most consequential decisions in car insurance is the choice between full coverage and liability-only coverage. Getting it wrong in either direction costs real money — either through unnecessarily high premiums or through financial exposure to an uncovered total loss.

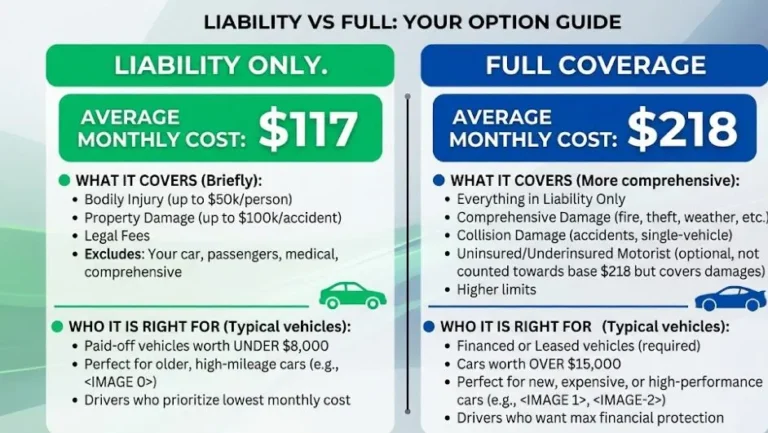

Liability Only — What It Is and Who It Is Right For

Liability coverage pays for damage you cause to other people — their vehicle, their medical expenses, their property. It does not pay to repair or replace your own vehicle. Every state except New Hampshire requires minimum liability coverage.

Erie and Auto-Owners offer the cheapest liability-only coverage on average: Erie at $445 a year and Auto-Owners at $540. GEICO is the cheapest national carrier for a liability-only policy at $619 a year, with the state minimum option even lower.

Liability only is appropriate when your vehicle’s actual cash value is low enough that the annual cost of adding collision and comprehensive coverage represents an unreasonable percentage of the car’s value. The general rule: if your car is worth less than $8,000 and you have no loan or lease on it, liability-only coverage may be the financially rational choice. Use Kelley Blue Book‘s private party value to determine your car’s actual cash value and compare the annual collision and comprehensive premium against it.

If your car is financed or leased, your lender requires full coverage — liability only is not a legal option until the loan is paid off.

Full Coverage — What It Is and Who Needs It

Full coverage means liability plus collision plus comprehensive. Collision pays for damage to your vehicle from a collision with another car or object. Comprehensive pays for damage from theft, fire, weather, animal strikes, and vandalism.

Full coverage is required by any lender or leasing company. It is the financially rational choice for any car worth more than $15,000 where the collision and comprehensive premium does not exceed approximately 10 percent of the car’s value annually. For most drivers with cars less than eight years old, full coverage is appropriate.

Travelers offers the cheapest full coverage rates at $175 per month among national carriers. Erie averages $159 per month regionally. The decision to maintain full coverage or drop to liability only should be revisited annually on older vehicles as their value depreciates.

The relationship between safety ratings and insurance cost is direct and meaningful — the 2021 Ford Escape’s strong IIHS safety ratings contribute to it being one of the more affordable compact SUVs to insure, a detail we cover in our 2021 Ford Escape complete guide alongside the vehicle’s full ownership cost picture including the recalls that any buyer in 2026 needs to know about.

Section 4 – What Drives Your Rate

The Eight Factors That Determine What You Pay

Understanding these factors gives you the ability to predict your quote before you shop and identify which variables you can change to reduce your premium.

Your Driving Record

Maintaining a clean driving record for three to five years without accidents or violations earns you discounts of 20 to 30 percent on most coverage types. Insurers view your history as the strongest predictor of future claims. A single at-fault accident raises rates by an average of 43 percent. A DUI raises rates by 35 to 155 percent depending on the carrier. The most powerful premium-reduction strategy available is also the simplest: drive carefully and maintain a clean record.

Your Age

Young drivers pay the highest rates — a 20-year-old pays $306 per month for coverage that costs a 35-year-old $139. Rates decline steadily from age 25 through approximately 65, then rise again as seniors age beyond 70. Age is a factor you cannot change, but understanding where you fall on the age curve explains a significant portion of why your rate is what it is.

Your Credit Score

In most states, insurance companies use a credit-based insurance score as a pricing factor. People with no credit pay 67 percent more than people with excellent credit on average. Improving your credit score is one of the highest-leverage long-term premium reduction strategies available in states where credit-based scoring is permitted. California, Hawaii, Massachusetts, and Michigan prohibit credit-based insurance scoring.

Your Location

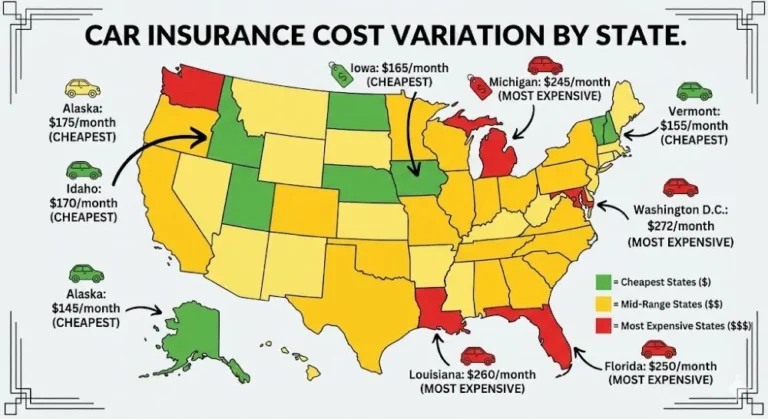

Where you garage your car overnight is a powerful pricing factor. The average car insurance rate for full coverage is $272 per month in Washington D.C., but drivers might only pay $145 per month for the same coverage in Alaska. Within states, urban ZIP codes consistently carry higher rates than rural areas. Location is a factor you can address by shopping companies that price your specific ZIP code favorably — pricing by geography varies significantly across carriers.

Your Vehicle

The car you drive affects your rate in two primary ways: its repair cost (expensive cars to repair carry higher collision and comprehensive premiums) and its safety rating (cars with high IIHS and NHTSA safety ratings carry lower premiums because they generate fewer and less severe claims). Certain car models cost more to insure than others — safe cars that cost less to repair, like minivans and family SUVs, are cheaper to insure than expensive, fast sports cars.

Your Coverage Level And Deductibles

Higher coverage limits cost more. Higher deductibles cost less. Raising your collision deductible from $500 to $1,000 typically reduces your collision premium by 10 to 15 percent. The trade-off is higher out-of-pocket exposure if you file a claim — choose the deductible level at which you can cover the cost without financial hardship.

Your Annual Mileage

Higher mileage means more exposure — more time on the road means more opportunity for an accident. Drivers logging under 7,500 miles annually should specifically ask for a low-mileage discount at every carrier they quote. The discount ranges from 5 to 15 percent at most carriers and is frequently not applied automatically without being specifically requested.

The vehicle you drive is one of the most underappreciated pricing factors in car insurance — and if you drive a pickup truck rather than a passenger car, the calculation is different enough that it deserves its own analysis. Our guide to cheapest truck insurance in 2026 covers every truck model’s insurance cost, the best companies for truck owners specifically, and strategies that apply particularly to pickup truck coverage.

Section 5 – Nine Strategies To Pay Even

What Actually Works Beyond Just Picking The Right Company

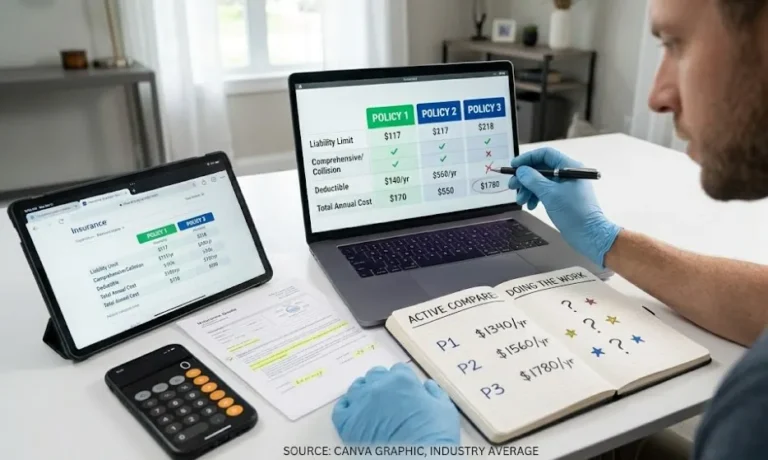

Strategy 1: Compare At Least Three To Five Quotes At Every Renewal

The most important action any driver can take is comparison shopping. Check if regional companies operate in your state. Regional insurers usually cost 28 to 34 percent below national averages in specific markets. Getting at least three to five quotes at every annual renewal exposes pricing changes that the windshield sticker and the renewal notice will never reveal. This thirty-minute annual exercise regularly produces savings of $300 to $900 per year for the same coverage.

Strategy 2: Bundle Home And Auto Insurance

State Farm emphasizes bundling discounts of 10 to 25 percent off for homeowners and households with multiple vehicles. Most major carriers offer comparable multi-policy discounts. For homeowners, comparing the combined total of a bundled home-plus-auto quote against maintaining separate policies at different carriers is consistently the highest-leverage bundling strategy. The bundle discount typically outweighs any rate advantage from keeping separate insurers.

Strategy 3: Enroll In A Telematics Program And Drive Well

GEICO’s DriveEasy, Progressive’s Snapshot, Travelers’ IntelliDrive, and State Farm’s Drive Safe and Save all offer discounts of 10 to 30 percent for drivers who allow monitoring of actual driving behavior. Progressive’s Snapshot program can reduce rates further if your driving habits are consistently low-risk. For smooth, careful drivers, these programs are effectively free premium reductions — the monitoring period runs 30 to 90 days, after which the discount is locked in at renewal.

Strategy 4: Insuring Two Or More Cars Saves 10 To 25 Percent

Insuring two or more cars on the same policy saves 10 percent to 25 percent. GEICO’s multi-vehicle discount is among the highest at 25 percent. The discount applies per additional vehicle, so households with three cars save more than households with two. If you currently insure multiple vehicles on separate policies — even for perceived convenience — consolidating them produces immediate savings.

Strategy 5: Raise Your Deductible

Increasing your collision deductible from $500 to $1,000 reduces the collision component of your premium by approximately 10 to 15 percent. Going to $2,000 can save 20 to 25 percent. This makes financial sense when your emergency fund can absorb the higher deductible cost in a claim scenario. On vehicles worth less than $15,000, the premium savings from a higher deductible frequently exceed the additional financial exposure over a three-to-five-year period.

Strategy 6: Ask Specifically For Every Discount You Qualify For

Insurance companies do not automatically apply all discounts you qualify for. Common discounts that drivers regularly miss include the good student discount for young drivers maintaining a 3.0 GPA or better, the defensive driving course discount for completing an approved course, the anti-theft device discount, the paid-in-full discount for paying annually, the paperless billing discount, and the loyalty discount for maintaining continuous coverage with the same carrier. Asking your agent or customer service representative for a discount review at renewal frequently produces $50 to $300 in additional annual savings.

Strategy 7: Maintain Continuous Coverage — Never Let It Lapse

A gap in car insurance coverage signals risk to every insurer and raises your rate by 15 to 30 percent at your next policy. Even a brief lapse creates a record that affects pricing for one to three years. If you sell a car and plan to be without a vehicle temporarily, a non-owner auto policy maintains your continuous coverage record at a minimal cost until your next vehicle purchase.

Strategy 8: Improve Your Credit Score Over Time

In states where credit-based insurance scoring is permitted, improving your credit score from poor to good can reduce your car insurance premium by 25 to 40 percent over the years of improvement. This is a long-term strategy rather than an immediate fix, but for drivers who plan to insure a vehicle for multiple years, the insurance dividend from credit improvement is real and compounding.

Strategy 9: Match Your Coverage To Your Vehicle’s Value Annually

Review your vehicle’s actual cash value every year and compare the annual cost of collision and comprehensive coverage against it. When the annual premium for those coverages exceeds approximately 10 percent of the car’s value — meaning you would need a claim every year for the insurance to break even mathematically — dropping to liability only becomes financially rational.

Section 6 – Regional Companies Worth Knowing

The Insurers You Have Probably Never Heard Of That Might Be Cheapest For You

National advertising budgets belong to national companies. But regional insurers — companies that operate in specific states or regions — often offer rates that the national carriers cannot match in their specific markets.

Check if regional companies operate in your state. Regional insurers usually cost 28 to 34 percent below national averages in specific markets.

COUNTRY Financial offers the cheapest average rate for car insurance at $46 per month in the markets where it operates, according to Compare.com data. Auto-Owners, at $48 per month average, is not far behind. North Star Mutual, Westfield Insurance, NJM Insurance, and Grange Insurance are all regional carriers that consistently appear among the cheapest options in their specific coverage areas.

The trade-off with regional carriers is availability, digital infrastructure, and claims network breadth. Regional carriers usually have lower pricing but fewer coverage options and may lack easy digital claims processes. For drivers who prioritize price above all else and are willing to manage a less sophisticated app or online portal, regional carriers represent the most consistently underexplored opportunity in car insurance shopping.

FAQ

Q: What is the cheapest car insurance company in 2026?

A: USAA is the cheapest car insurance company overall in 2026, with full coverage averaging $1,542 per year and liability-only averaging $412 per year — available only to military members, veterans, and immediate family. For drivers who do not qualify for USAA, Travelers is the cheapest national carrier for full coverage at $1,665 per year, and GEICO is the cheapest for liability-only at $494 per year. Regional carriers Erie Insurance and Auto-Owners are cheaper than all national carriers in the states where they operate.

Q: How much is car insurance per month on average in 2026?

A: The national average for full coverage car insurance is $2,611 per year or $218 per month in 2026. Liability-only coverage averages $1,407 per year or $117 per month. These are national averages — your actual rate will be higher or lower based on your age, driving record, location, vehicle, credit score, and coverage level. Drivers in some states pay significantly more or less than these averages.

Q: Is GEICO actually the cheapest car insurance?

A: GEICO is the cheapest large auto insurance company for liability-only coverage at $41 per month nationally. For full coverage, Travelers at $139 per month is cheaper than GEICO at $171 per month. GEICO is competitive for drivers with clean records and standard profiles but is not the cheapest in all situations — after a DUI, GEICO’s rates increase by 155 percent, making it one of the more expensive options for that profile. Always compare GEICO against Travelers and your regional options before assuming GEICO is cheapest for your specific situation.

Q: How much cheaper is USAA than other companies?

A: USAA’s full coverage averages $1,542 per year — $1,069 per year less than the national average of $2,611. For qualified drivers, that is an $89 per month savings compared to the national average and approximately $570 per year less than Travelers, the next cheapest national carrier. Over a five-year vehicle ownership period, the savings from USAA compared to the national average compound to more than $5,000.

Q: What is the cheapest car insurance for a teenager in 2026?

A: The cheapest car insurance for teenage drivers is from Erie, USAA, and GEICO. These companies charge average 17-year-old drivers as little as $1,325 per year for minimum coverage, compared to the national average of $2,339 per year for the same profile. The most effective cost-reduction strategy for teen drivers is adding them to the family policy rather than purchasing a standalone policy — and claiming the good student discount for students maintaining a 3.0 GPA or better.

Q: What is the cheapest car insurance after a DUI?

A: Progressive offers the cheapest car insurance after a DUI among major national carriers, averaging $3,625 per year. Progressive is the cheapest company after a DUI across most states. GEICO is among the worst choices post-DUI, raising rates by up to 155 percent. After any major violation, comparison shopping is essential — the difference between carriers after a DUI can be $1,500 to $2,000 per year for identical coverage.

Q: Does your credit score affect car insurance rates?

A: Yes — in most states. Insurance companies use a credit-based insurance score as a pricing factor in 46 states. People with poor credit pay 60 to 80 percent more than those with excellent credit on average. States that prohibit credit-based insurance scoring include California, Hawaii, Massachusetts, and Michigan. In all other states, improving your credit score over time is one of the most effective long-term strategies for reducing your car insurance premium.

Q: How do I get the cheapest car insurance possible?

A: The most effective approach combines several strategies simultaneously: compare quotes from at least three to five companies at every renewal, include regional carriers in your comparison, bundle home and auto if you own, enroll in a safe driver telematics program, increase your deductible to the level your emergency fund can absorb, request a discount review at every renewal, and maintain continuous coverage without lapses. Combining multiple strategies consistently produces savings of $400 to $1,200 per year beyond what any single strategy achieves alone.

The Bottom Line

The cheapest car insurance company in 2026 is USAA — for those who qualify. The cheapest for everyone else is Travelers for full coverage and GEICO for liability only — until your specific driver profile, location, and vehicle make a regional carrier or a different national option cheaper for you specifically.

That last clause is the entire argument for shopping rather than assuming. The car insurance market is one of the few major consumer financial markets where the price for identical products varies by more than 100 percent across providers. The tools to compare those prices take thirty minutes annually. The savings from using those tools regularly run $300 to $1,200 per year. The return on that time investment is extraordinary — and yet most Americans spend more time comparing grocery prices than comparing insurance quotes.

Get three quotes. Compare identical coverage levels. Include regional carriers. Run the comparison every year at renewal. The number on your policy will be lower. The protection will be identical. The only thing that changes is what you keep.

Editorial Note

This article was written and reviewed in March 2026. All company rate data is sourced from NerdWallet, U.S. News, MoneyGeek, Insurance.com, CarInsurance.com, and WalletHub. All rates represent averages for a standard driver profile and are for comparison purposes only — your actual rate will vary based on your driver profile, vehicle, location, and coverage selections. Company rate rankings may vary based on your specific situation. Always obtain quotes directly from insurance companies or licensed agents for accurate pricing specific to your circumstances.

0 Comments